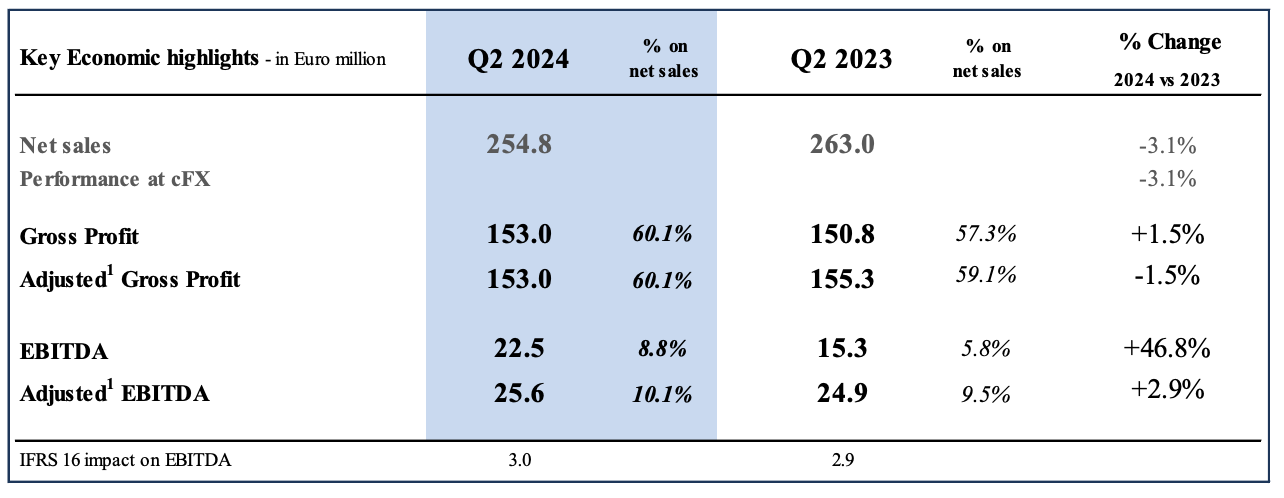

Sàfilo Group S.p.A. reported second quarter net sales amounted to €254.8 million, down 3.1 percent both at constant and current exchange rates compared to €263.0 million recorded in Q2 2023.

The performance of the period was said to reflect two story lines. In one story, it was the reduction in sales of Jimmy Choo, which had a stronger impact than in Q1 on the performance of North America and Europe. In the other story line, the business benefitted from the double-digit growth delivered by Carrera and David Beckham, and the ongoing momentum of Carolina Herrera and Marc Jacobs. The quarter was said to instead be challenging for Smith, due to a still subdued business environment in stores, and for Polaroid, which was affected by the poor weather conditions in Europe.

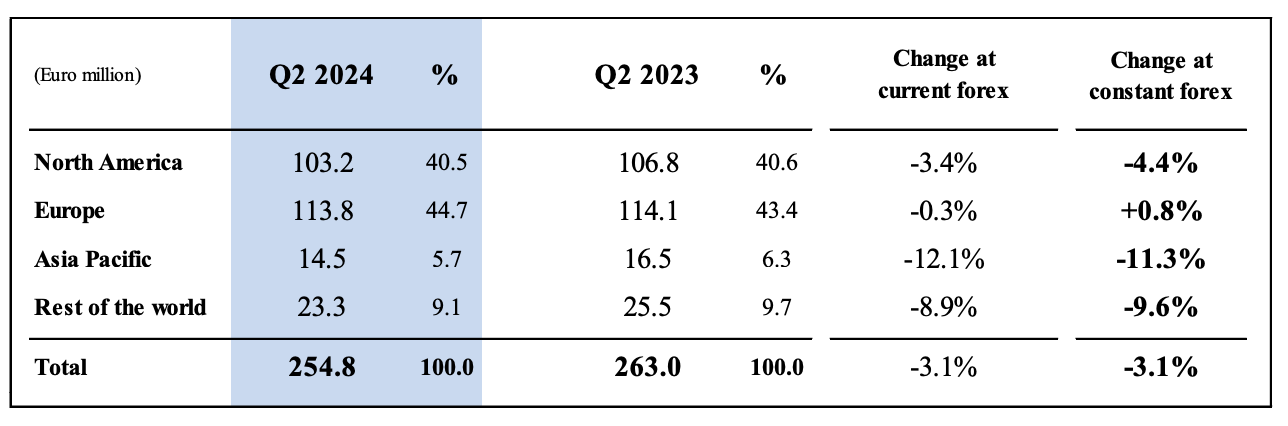

Second Quarter Region Review North America

North America

Sales in North America amounted to €103.2 million in the quarter, down 4.4 percent at constant exchange rates and 3.4 percent at current exchange rates compared to Q2 2023. Excluding the Jimmy Choo negative impact, sales performance was said to be substantially stable compared to last year, driven by an eyewear business that showed a recovery, and the sport shops channel that was still subdued.

In the United States, Q2 was a positive quarter for Carrera, driven by the success of its new woman collections, supporting the brand’s productivity in store and its further expansion in the market, and for some of the Group’s core licenses, namely David Beckham, Carolina Herrera, Marc Jacobs and Tommy Hilfiger, which saw distribution grow double-digits.

The company called out that Smith’s wholesale revenues of helmets were hampered by lower re-orders of winter products due to a late start to the ski season and a bike business still partially overstocked at the point of sale. Smith’s performance remained very positive in its direct-to-consumer (DTC) channel, which continued to benefit from greater responsiveness of the end consumer and a more favorable product mix.

Europe

Sales in Europe amounted to €113.8 million in Q2, up 0.8 percent at constant exchange rates and substantially unchanged, at down 0.3 percent, at current exchange rates compared to Q2 2023. The deceleration compared to the first quarter of the year was explained by poor weather conditions that affected the sell-out of most channels between May and June, coupled with the higher impact from the exit of Jimmy Choo.

The positive sales trend reportedly continued to be driven by the French market, led by a solid prescription frames business, and by the growth of Central and Eastern European markets. In Germany, both the internet pure player (IPP) channel and sales at some major optical chains recorded positive performance.

Asia Pacific

Sales in Asia Pacific amounted to €14.5 million in the quarter, down 11.3 percent at constant exchange rates and 12.1 percent at current exchange rates. The performance of the period reflected the weak sales trend at distributors in Southeast Asia and the challenging comparison with Q2 2023 (+38 percent compared to Q2 2022), which mitigated the still positive performance of China, where Ports and Polaroid led the market growth.

Rest of World

Sales in the Rest of the World amounted to €23.3 million, down 9.6 percent at constant exchange rates and 8.9 percent at current exchange rates compared to Q2 2023. In the period, sales in Latin America slowed down, mainly due to a weak travel retail business, while in IMEA positive trends in the Middle Eastern and African markets were countered by some sales normalization in India.

Income Statement Highlights

Safilo said it made further progress in margin expansion in the second quarter, continuing to post an improvement both at the industrial and operating level. As seen in the first quarter, the main positive drivers of the period were the higher supply chain efficiency and the lower depreciation resulting from the industrial restructuring that took place in Italy in 2023, coupled with a positive price/mix effect on sales. In addition, in Q2 the dilution effect of phase-out sales became less impactful than in the first quarter.

Despite the still unfavorable operating leverage, the company said the Q2 operating performance recorded a more significant year-on-year margin recovery than Q1, benefitting in particular from the ongoing normalization of IT investments and marketing and advertising expenses.

Gross profit amounted to €153.0 million, declining 1.5 percent, compared to the adjusted gross profit recorded in Q2 2023. Gross margin improved 100 basis points to 60.1 percent of sales from the adjusted level of 59.1 percent recorded in Q2 2023.

Selling and marketing, general and administrative expenses decreased by around 2 percent compared to Q2 2023, while their incidence on sales moderately increased due to an unfavorable operating leverage.

Adjusted EBITDA amounted to €25.6 million, up 2.9 percent compared to Q2 2023, while the adjusted EBITDA margin improved by 60 basis points, to 10.1 percent from 9.5 percent recorded in Q2 2023.

First Half Highlights

Safilo closed the first half of 2024 with net sales of €532.0 million, down 2.4 percent at constant exchange rates and 3.3 percent at current exchange rates compared to €550.1 million recorded in H1 2023.

- Sales in North America totaled €217.6 million, down 5.9 percent at constant exchange rates and 6.0 percent at current exchange rates compared to €231.5 million recorded in H1 2023.

- Sales in Europe totaled €239.1 million, up 3.4 percent at constant exchange rates and 1.4 percent at current exchange rates compared to €235.7 million recorded in H1 2023.

- Sales in Asia Pacific totaled €26.4 million, down 5.6 percent at constant exchange rates and 7.5 percent at current exchange rates compared to €28.6 million recorded in H1 2023.

- Sales in the Rest of the World totaled €48.8 million, down 11.3 percent at constant exchange rates and 10.2 percent at current exchange rates compared to €54.4 million recorded in H1 2023.

Gross profit amounted to €319.2 million, slightly declining by 1.4 percent, compared to the adjusted gross profit recorded in H1 2023, while the gross margin improved by 120 basis points, reaching 60.0 percent from the adjusted level of 58.8 percent in H1 2023.

Selling and marketing, general and administrative expenses declined by around 2.5 percent compared to H1 2023, while their incidence on sales increased due to an unfavorable operating leverage.

Adjusted EBITDA amounted to €57.6 million, up 0.5 percent compared to H1 2023, while the adjusted EBITDA margin improved by 40 basis points, to 10.8 percent of sales from 10.4 percent recorded in H1 2023.

Adjusted operating result amounted to €37.6 million, up 7.2 percent compared to H1 2023, while the adjusted operating margin improved by 70 basis points, to 7.1 percent of sales from 6.4 percent recorded in H1 2023.

The Group’s adjusted net result equalled €24.2 million compared to €6.9 million recorded in H1 2023, a result that was last year affected by a charge of €8.6 million, due to the revaluation of the liability for options on the interest in Blenders. In H1 2024, net financial charges decreased to €6.9 million from €9.4 million in H1 2023, mainly due to a lower average Group net debt.

Balance Sheet and Cash Flows

In the first semester (first half), the cash flow from operating activities reached €27.3 million, posting an improvement compared to €21.1 million recorded in the same period of 2023. In the second quarter, the cash generation of around €21 million, was driven by the positive economic performance of the period, also including the settlement of a nonrecurring cost related to a terminated license agreement, and by a cash generation from working capital also due to a reduction of inventories.

The cash flow for investing activities grew to €41.1 million, mainly explained by the investment made by the Group for the perpetual license of the Eyewear by David Beckham.

On June 30, 2024, the Group’s net debt stood at €100.4 million (€62.6 million pre-IFRS 16, corresponding to a financial leverage, also pre-IFRIC SaaS, of 0.7x), from €82.7 million (€43.7 million pre-IFRS 16) recorded as of December 31, 2023, and €103.0 million (€61.7 million pre-IFRS 16) at the end of June 2023.

The key components of the Group’s net debt at the end of June 2024 were the following:

- A long-term debt position of €102.5 million, made of bank loans for €73.7 million, related to the Credit Facility signed in September 2022, and an IFRS-16 effect for €28.8 million;

- A short-term debt position of €39.5 million, made of bank loans for €30.5 million, related to the Credit Facility, and an IFRS-16 effect for €9.0 million; and

- A cash position of €41.6 million.

Safilo Chief Executive Officer Angelo Trocchia commented:

“This first semester ended by confirming the main market dynamics and trends by brand recorded in the first quarter. In Europe, the market was positive despite a second quarter slowed down by poor weather conditions. In North America, the eyewear business showed an improvement, while Smith sports business remained subdued in physical stores.

“In the second quarter, total sales performance was more negatively impacted by the Jimmy Choo exit, while benefitting from the strong momentum of Carrera and David Beckham, which continued to win consumers’ appreciation and new space in stores.

“Notwithstanding a business environment which remained challenging, the quarter was satisfactory for us at the economic level, with the gross margin confirming its 60 percent level and the adjusted EBITDA margin improving to a larger extent than in the first quarter.

“We approached this first half of the year focused on our medium and long-term goals, reinvesting the positive operating cash flow in the continuous strengthening and development of our brand portfolio. By transforming David Beckham’s partnership into a perpetual license, we have permanently secured one of the most promising and profitable brands of our portfolio. Today, our home brands, together with the Eyewear by David Beckham, already account for around 50 percent of sales, another important milestone that allows us to face with clarity and pragmatism both the challenges and opportunities of our industry.”

Image courtesy Smith Optics, Data courtesy Sàfilo Group S.p.A.